WEEK 2

Consumers and Business

The Role of Consumers in the Economy

You will learn about:

You will learn to:

Examine economic issues

Apply economic skills

Traditional economics sets out some basic premises. Let's think these through and see where they are happening in our everyday lives.

You will learn about:

- why economists believe in the concept of consumer sovereignty,

- what influences what you buy.

You will learn to:

Examine economic issues

- assess the extent to which consumer sovereignty is achieved in a variety of markets

- examine the impact of income on the spending and saving decisions of individuals

Apply economic skills

- analyse the impact of changes in consumer income levels on the types of production within the economy

Traditional economics sets out some basic premises. Let's think these through and see where they are happening in our everyday lives.

- The consumer is king (or queen) because they use their purchasing power to tell producers of goods and services what and how much to produce.

- Our income (Y) is divided into what we spend (C) and what we save (S).

- We spend or save according to our age and income.

- In the economy as a whole, as income rises the level of saving increases.

- A variety of factors influence individuals' consumption choices. These include: income, price, the price of substitutes and complements, preferences or tastes and advertising.

Where does this idea begin?

Do you feel like a king or queen when you go to the local supermarket or surf shop? What influence do you really have on what Woolworths, IGA or Coles stock in their aisles? Where did the concept of consumer sovereignty come from?

It relies on the assumption that consumers are rational and will buy the cheapest good.

PRICE IS AN IMPORTANT DETERMINANT OF WHETHER A GOOD OR SERVICE GETS SOLD, BUT IS THIS A TRUE AND RELIABLE REFLECTION OF A GOOD'S VALUE?

In the following article, the author discusses how economist Mariana Mazzucato has gone back to the roots of economics to find out how prices alone came to determine value.

If the price you pay isn't the real cost, what's really happening when you purchase a good?

Here's an excerpt:

"Value theory was at the heart of economics when the discipline was born. Adam Smith, writing during the industrial revolution, believed that the value of a commodity comes from the hands that made it — workers. With labour as his starting point, Smith articulated a theory of production, and from there, a theory of economic growth. Without a clear idea of what creates value, anything that gets bought and sold on the market is counted as productive. Conversely, any activity that can’t be priced can’t be seen as economically productive.

As a consequence, the traditional models make it difficult for economists and policy-makers to distinguish economic activity that creates value from activity primarily engaged in value extraction, or rent-seeking. According to Mazzucato, an overemphasis on price risks misidentifying “making” with “taking.” "

In the following article, the author discusses how economist Mariana Mazzucato has gone back to the roots of economics to find out how prices alone came to determine value.

If the price you pay isn't the real cost, what's really happening when you purchase a good?

Here's an excerpt:

"Value theory was at the heart of economics when the discipline was born. Adam Smith, writing during the industrial revolution, believed that the value of a commodity comes from the hands that made it — workers. With labour as his starting point, Smith articulated a theory of production, and from there, a theory of economic growth. Without a clear idea of what creates value, anything that gets bought and sold on the market is counted as productive. Conversely, any activity that can’t be priced can’t be seen as economically productive.

As a consequence, the traditional models make it difficult for economists and policy-makers to distinguish economic activity that creates value from activity primarily engaged in value extraction, or rent-seeking. According to Mazzucato, an overemphasis on price risks misidentifying “making” with “taking.” "

Economist Mariana Mazzucato has gone back to the roots of economics to find out how prices alone came to determine value.

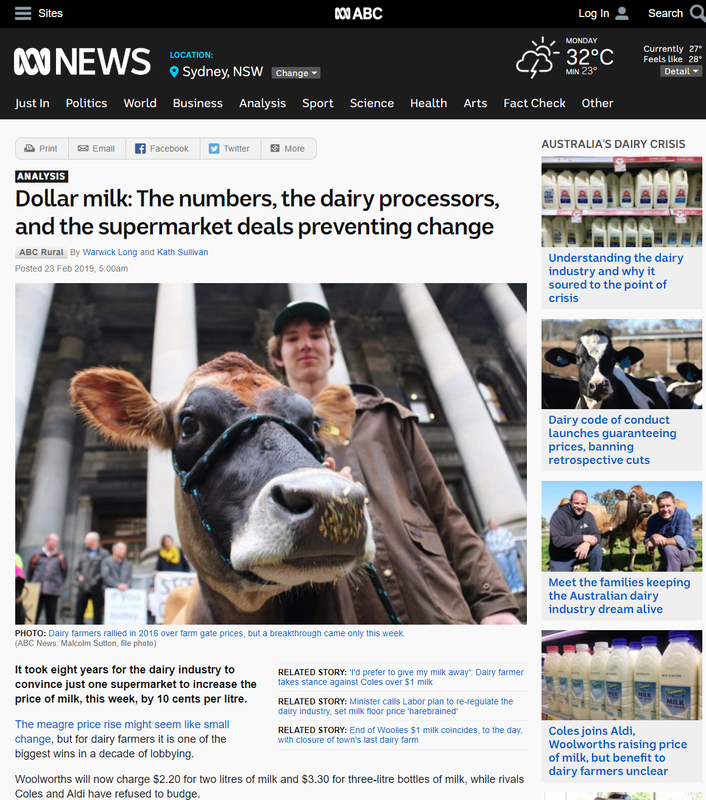

How much is $2 milk costing you?

The supermarkets' recent price decisions

Announcements by Coles

2.1 On 26 January 2011, Coles announced as part of its 'Down Down' campaign that the price of Coles Brand fresh milk will be cut by as much as 33 per cent, to $2 for a two litre bottle. The Coles Brand low fat milk was also reduced to $2 for a two litre bottle, eliminating the slight premium that was previously charged. In its media release announcing the price changes, Coles stated:

Coles is not reducing the price it pays to its milk processors either so this move will not impact them or the dairy farmers who supply them. In fact both farm gate milk prices and contract prices with processors recently increased. Coles is fully absorbing the price cut, bringing great value to customers whilst supporting Australian dairy farmers.

2.2 At the same time Coles announced it would phase out its Smart Buy range of milk, leaving one generic Coles brand sold in the milk market. Coles noted that customers that previously bought the Smart Buy branded milk would receive a slight discount under the new pricing structure:

As well as lowering prices on Coles Brand fresh milk, Coles is also phasing out its Smart Buy fresh milk in order to simplify the range for customers. Customers who currently choose Smart Buy milk will also save money** by switching to Coles Brand milk at the new low price of $2 for two litres—the lowest price in store for any fresh milk.

**Smart Buy 2 litre full cream fresh milk was priced at $2.09 in every State so customers switching from this product to 2 litre Coles Brand fresh milk (full cream or lite) at the new regular low price of $2 are saving 4%.

[2]

2.3 On 3 January 2011, Coles announced reductions in the prices of Coles brand butter and cream, and various brands of olive oil.[3] The 'Down Down' campaign has since been extended to cover a number of other grocery items, such as breakfast cereals and tea. Other private label products, such as eggs, had also been heavily discounted before the milk price cuts.[4]

Announcements by Coles

2.1 On 26 January 2011, Coles announced as part of its 'Down Down' campaign that the price of Coles Brand fresh milk will be cut by as much as 33 per cent, to $2 for a two litre bottle. The Coles Brand low fat milk was also reduced to $2 for a two litre bottle, eliminating the slight premium that was previously charged. In its media release announcing the price changes, Coles stated:

Coles is not reducing the price it pays to its milk processors either so this move will not impact them or the dairy farmers who supply them. In fact both farm gate milk prices and contract prices with processors recently increased. Coles is fully absorbing the price cut, bringing great value to customers whilst supporting Australian dairy farmers.

2.2 At the same time Coles announced it would phase out its Smart Buy range of milk, leaving one generic Coles brand sold in the milk market. Coles noted that customers that previously bought the Smart Buy branded milk would receive a slight discount under the new pricing structure:

As well as lowering prices on Coles Brand fresh milk, Coles is also phasing out its Smart Buy fresh milk in order to simplify the range for customers. Customers who currently choose Smart Buy milk will also save money** by switching to Coles Brand milk at the new low price of $2 for two litres—the lowest price in store for any fresh milk.

**Smart Buy 2 litre full cream fresh milk was priced at $2.09 in every State so customers switching from this product to 2 litre Coles Brand fresh milk (full cream or lite) at the new regular low price of $2 are saving 4%.

[2]

2.3 On 3 January 2011, Coles announced reductions in the prices of Coles brand butter and cream, and various brands of olive oil.[3] The 'Down Down' campaign has since been extended to cover a number of other grocery items, such as breakfast cereals and tea. Other private label products, such as eggs, had also been heavily discounted before the milk price cuts.[4]

Who is ultimately responsible for $2 milk?

Consider this...

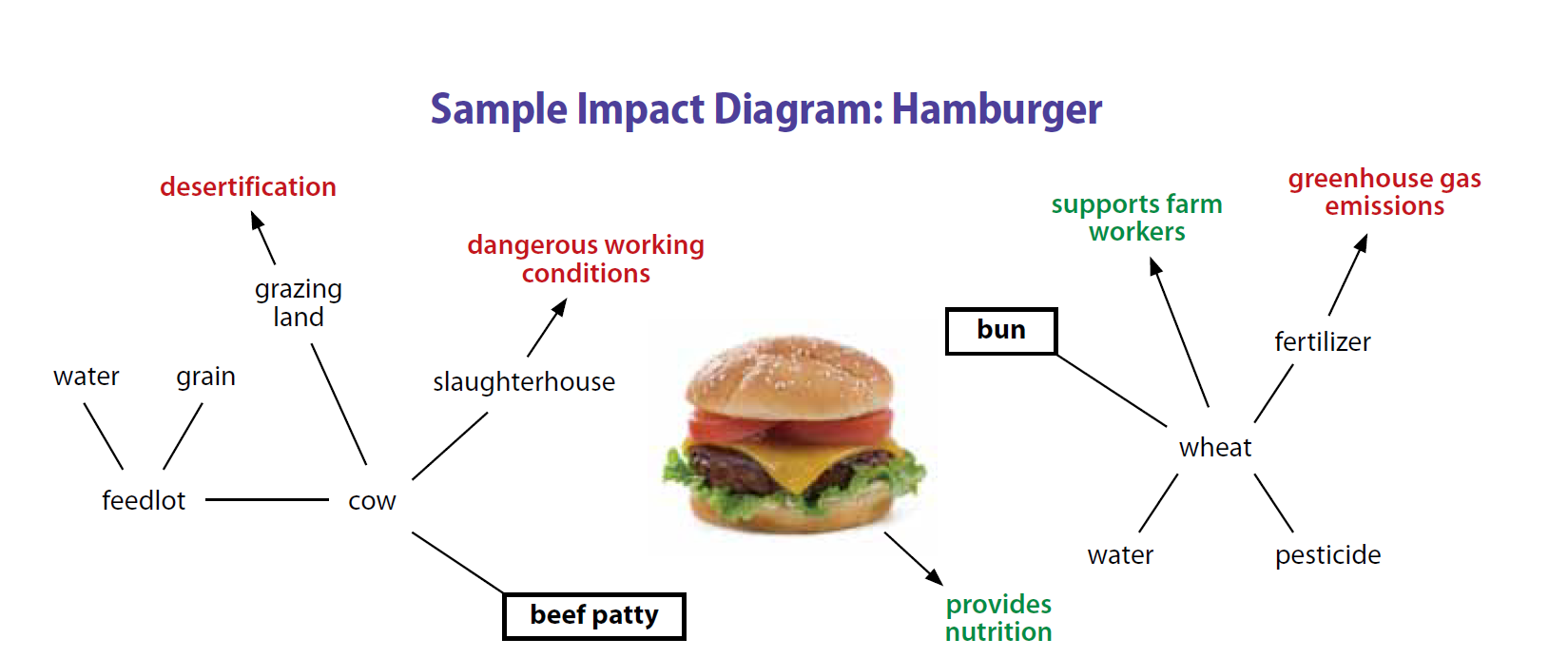

Does your $11.10 Big Mac really cost $11.10? When you buy this meal what are the impacts? Would you change your consumption patterns if everything you bought was mapped like this?

Reference: www.facingthefuture.org

Graphic images on cigarette packaging showing the serious impacts on individual's health had some success in changing people's consumption patterns but plain packaging was more successful. Can you suggest why plain packaging stopped people smoking rather than showing graphic images?

When governments 'buy' products through subsidies, what are the impacts?

We need to go beyond mere statistical regularities to understand,

for example, how the world of money affects the supply of goods

and services. We need to investigate how economics influences our

political choices, and how those choices that feed back to

economics. And we must recognize that economic behavior is

shaped not only by prices and regulation but also by social norms

that are woven into our psyche and influence our individual choices

– and, through those choices, the wellbeing of our communities,

countries, and the world.

Kaushik Basu in "The assumptions that underpin modern economics need reviewing. This is why." (3 Jan, 2020, WEF)

Professor of Economics, Cornell University

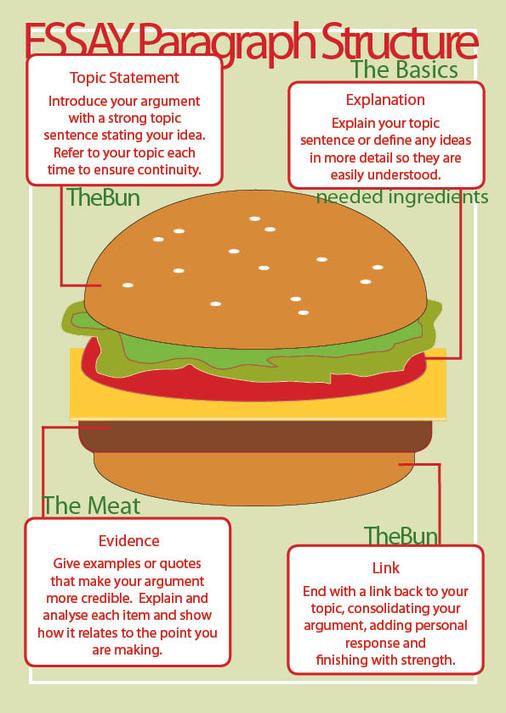

Can you assess the extent to which consumer sovereignty is achieved in a variety of markets?

|

Using the Topic, Explanation, Evidence and Link structure, write a paragraph responding to this question.

Here's what a good one looks like (WAGOLL): Consumer sovereignty describes how consumer preferences will ultimately determine what gets produced and distributed in the economy. The reality of this concept is limited however, as the economy is complex and presents a number of limiting factors on the theory. Not all consumers have access to the same levels of income and at times, they act irrationally in an economic sense. When Apple produced the first iPhone, they were not responding to consumers' preferences, they were innovating. Consumer sovereignty is not a dominate factor in today's globalised market and is limited in its ability to describe what consumers buy and what producers create. |

Consumer Sovereignty

This concept has limited applicability when we look at the world we live in. There are many other factors that determine what we have available in our local shops. Our choices are not always the sovereign choice. The next section looks at other factors that feed into consumer choices that create the economy.

Can you examine the impact of income on the spending and saving decisions of individuals?

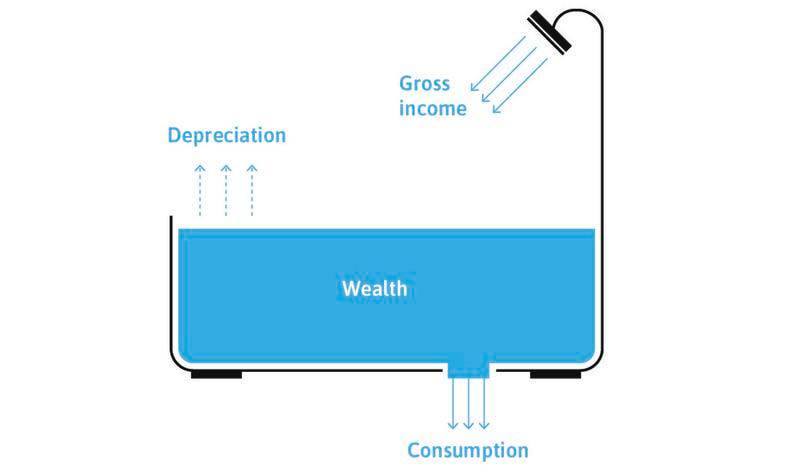

Y = C + S

Income is the amount of money you receive over some period of time, whether from market earnings, investment, of from the government.

Since it is measured over a period of time (such weekly or yearly), it is a flow variable. Wealth is a stock variable, meaning that it has no time dimension. At any moment of time it is just there. In this topic we only consider after-tax income, also known as disposable income.

To remember the difference between wealth and income, think of filling a bathtub, as below. Wealth is the amount (stock) of water in the tub, while income is the flow of water into the tub. The inflow is measured by litres (or gallons) per minute; the stock of water is measured by litres (or gallons) at a particular moment in time.

Since it is measured over a period of time (such weekly or yearly), it is a flow variable. Wealth is a stock variable, meaning that it has no time dimension. At any moment of time it is just there. In this topic we only consider after-tax income, also known as disposable income.

To remember the difference between wealth and income, think of filling a bathtub, as below. Wealth is the amount (stock) of water in the tub, while income is the flow of water into the tub. The inflow is measured by litres (or gallons) per minute; the stock of water is measured by litres (or gallons) at a particular moment in time.

Reference: https://core-econ.org/the-economy/book/images/web/figure-10-01.jpg

Reference: https://www.tutor2u.net/economics/reference/household-saving

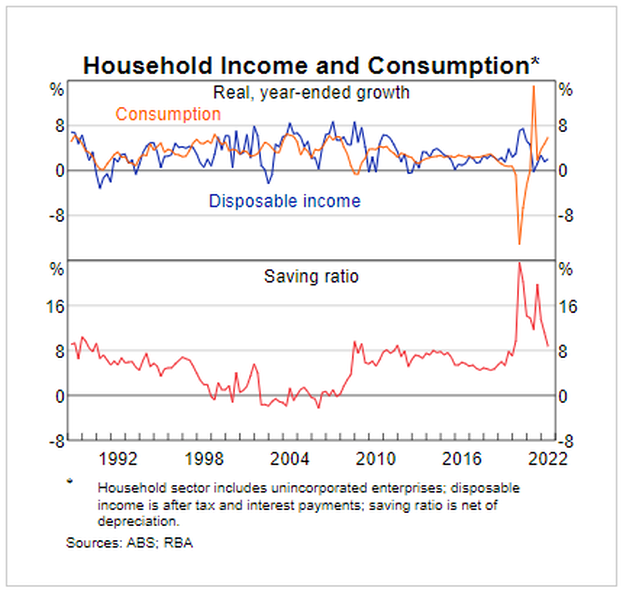

What factors affect how much of their income people save?

What factors affect how much of their income people save?

- Real interest rate on savings deposits – i.e. the return on savings adjusted for inflation

- Expectations of future income and job security / all linked to consumer confidence

- Availability of credit – borrowing to finance extra spending counts as dis-saving

- Taxation of saving e.g. tax efficient savings schemes and tax relief on occupational pensions such may encourage people to put away more of their disposable income

- The need to save to repay debt – e.g. property owners stuck in negative equity where their house is worth less than their mortgage debt or families that need to cut their debts on credit cards

- A need to save to build up a deposit for a mortgage, pay school and university fees, and save for retirement in an occupational pension scheme

- The availability of savings institutions such as banks and our trust in those institutions.

Can you analyse the impact of changes in consumer income levels on the types of production within the economy?

As a college student you work at a part-time job, but your parents also send you a monthly “allowance.” Suppose one month your parents forgot to send the check. Show graphically how your budget constraint is affected. Assuming you only buy normal goods, what would happen to your purchases of goods?

Consider these mindgames:

1. Although a person's income will generally increase their demand for goods, there are some goods for which demand will fall when income rises. These are called inferior goods, can you suggest some examples?

2. There are some goods that actually experience a fall in demand when price decreases called giffen goods. Identify examples and why this phenomena would occur.

What are the bigger influences on consumer income levels?

Test your knowledge:

Read about the Novel-Coronavirus:

Opinion

Global Economy

Coronavirus will hit global growth

China’s place in the world economy has grown dramatically since the US triggered earlier recessions

RANA FOROOHAR

Reference: https://www.ft.com/content/8be84270-4430-11ea-a43a-c4b328d9061c

Last week, I enjoyed a city break in Istanbul with my teenage daughter. It was made even better by the fact that we were upgraded to a €1,000 room for only €250 — in large part because our hotel, which expected to be booked solid by wealthy Chinese holidaymakers, was nearly empty.

Everywhere around the city, merchants displaying “Happy Chinese New Year” signs were even more aggressive than usual in hawking their wares to passing tourists. There weren’t many of us. “It’s coronavirus,” said the concierge. “Last year around this time, we were packed. This year, nothing.”

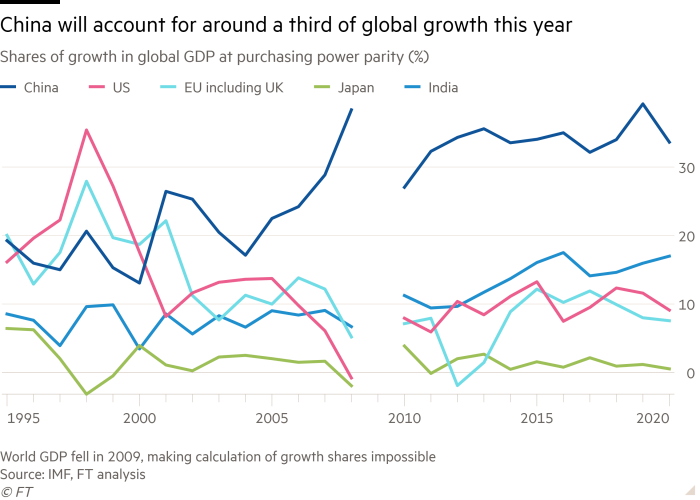

We might be about to see something new: a global slowdown led by China, rather than the US. The past four global recessions have been triggered by American consumers. But China’s place in the global economy has grown dramatically over that time. China today accounts for about one-third of global growth, a larger share than the US, Europe and Japan combined.

While there is no doubt that growth has slowed in recent years, the base from which China is growing has exponentially increased. As China bull Andy Rothman, an investment strategist with Matthews Asia, notes, while gross domestic product growth was at 9.4 per cent a decade ago, the base for last year’s 6.1 per cent growth was 188 per cent larger than 10 years ago. It means that what Chinese consumers and workers do today matters a lot more than it once did. “Chinese consumers drove global economic growth in 2019,” says Mr Rothman, just as they did for several years previously.

Opinion

Global Economy

Coronavirus will hit global growth

China’s place in the world economy has grown dramatically since the US triggered earlier recessions

RANA FOROOHAR

Reference: https://www.ft.com/content/8be84270-4430-11ea-a43a-c4b328d9061c

Last week, I enjoyed a city break in Istanbul with my teenage daughter. It was made even better by the fact that we were upgraded to a €1,000 room for only €250 — in large part because our hotel, which expected to be booked solid by wealthy Chinese holidaymakers, was nearly empty.

Everywhere around the city, merchants displaying “Happy Chinese New Year” signs were even more aggressive than usual in hawking their wares to passing tourists. There weren’t many of us. “It’s coronavirus,” said the concierge. “Last year around this time, we were packed. This year, nothing.”

We might be about to see something new: a global slowdown led by China, rather than the US. The past four global recessions have been triggered by American consumers. But China’s place in the global economy has grown dramatically over that time. China today accounts for about one-third of global growth, a larger share than the US, Europe and Japan combined.

While there is no doubt that growth has slowed in recent years, the base from which China is growing has exponentially increased. As China bull Andy Rothman, an investment strategist with Matthews Asia, notes, while gross domestic product growth was at 9.4 per cent a decade ago, the base for last year’s 6.1 per cent growth was 188 per cent larger than 10 years ago. It means that what Chinese consumers and workers do today matters a lot more than it once did. “Chinese consumers drove global economic growth in 2019,” says Mr Rothman, just as they did for several years previously.

No wonder people in the hospitality, tourism, travel and retail industries are seriously worried about the impact of the coronavirus. Chinese travellers are especially valuable because they tend to stay longer and spend more than those from other countries — in the US, for example, they stayed an average of 18 days and spent $7,000 per visit last year, according to a 13D Global Strategy and Research report.

While Chinese spending in the US was already slowing because of the trade war, Asia and Europe will now feel its loss as well. That will have knock-on effects in areas that are dependent on tourism: retail, restaurants, luxury goods and services of all kinds.

Goldman Sachs estimates a hit of 0.4 percentage points to China’s 2020 growth and a similar drag on US growth in the first quarter. Optimists will note that during the Sars outbreak in 2003, Chinese growth dipped only briefly before rebounding to a robust 10 per cent. But back then, China accounted for just 4 per cent of global growth, compared with 16 per cent today. Consumer spending wasn’t nearly as developed, and Chinese tourism was still mainly inbound. “Consequently . . . the negative impact on global growth could be higher than in 2003,” noted an ING report on the topic.

While Chinese spending in the US was already slowing because of the trade war, Asia and Europe will now feel its loss as well. That will have knock-on effects in areas that are dependent on tourism: retail, restaurants, luxury goods and services of all kinds.

Goldman Sachs estimates a hit of 0.4 percentage points to China’s 2020 growth and a similar drag on US growth in the first quarter. Optimists will note that during the Sars outbreak in 2003, Chinese growth dipped only briefly before rebounding to a robust 10 per cent. But back then, China accounted for just 4 per cent of global growth, compared with 16 per cent today. Consumer spending wasn’t nearly as developed, and Chinese tourism was still mainly inbound. “Consequently . . . the negative impact on global growth could be higher than in 2003,” noted an ING report on the topic.

It is not only Chinese consumers who may drive a slowdown. The Hubei region is a huge area for supply chains. Travel bans have made it difficult for people to work and to keep factories running. It is possible that with enough supply chain disruption China won’t be able to meet its US trade deal purchasing commitments.

That would of course have a geopolitical impact, particularly in sectors including technology, which are still among those most closely linked to Chinese businesses, despite the decoupling that is already taking place between the US and the Middle Kingdom (a trend that the “phase one” trade deal won’t change). If the tech sector starts to look wobbly, that might affect energy and material inputs, and, in turn, be the catalyst for the larger market correction that many of us have been expecting for some time.

All this makes the outbreak of the virus exactly the sort of unexpected trigger event that many market participants have been fretting about — they are already worried about declining US corporate profit margins, record debt, liquidity issues and negative yields.

Of course, it is possible that the markets will shrug it all off for a while longer. Perhaps Donald Trump will be able to claim, just in time for elections in November, that he was US president when the Dow reached 30,000. But that potential market high would have been driven by monetary policy and deficit spending rather than any more productive White House strategy.

This underscores a wider point: whatever happens with coronavirus, the US has missed an opportunity, not just under Mr Trump but ever since the 2008 financial crisis, to reset its growth strategy, ideally to one based more on income growth than asset price inflation. That is the only way to assure economic security over the longer term.

China, too, has been overly dependent on debt during the post-financial crisis period. It has brewed up its own bubbles in everything from real estate to provincial bonds. Consumption and labour markets were weakening even before coronavirus hit. Trust in governance, already waning under President Xi Jinping, has taken a new hit with the party’s initial downplaying of the crisis.

And yet, whatever toll the virus may eventually take on global growth, the fact that recession fears, which seemed a non-issue only a week ago, are now back says something very important.

The US still matters a lot in the global economy, but much less than it used to. China, on the other hand, matters much more. Just how much will be measured as the story of coronavirus plays out in the weeks and months ahead.

[email protected]

Follow Rana Foroohar with myFT and on Twitter

That would of course have a geopolitical impact, particularly in sectors including technology, which are still among those most closely linked to Chinese businesses, despite the decoupling that is already taking place between the US and the Middle Kingdom (a trend that the “phase one” trade deal won’t change). If the tech sector starts to look wobbly, that might affect energy and material inputs, and, in turn, be the catalyst for the larger market correction that many of us have been expecting for some time.

All this makes the outbreak of the virus exactly the sort of unexpected trigger event that many market participants have been fretting about — they are already worried about declining US corporate profit margins, record debt, liquidity issues and negative yields.

Of course, it is possible that the markets will shrug it all off for a while longer. Perhaps Donald Trump will be able to claim, just in time for elections in November, that he was US president when the Dow reached 30,000. But that potential market high would have been driven by monetary policy and deficit spending rather than any more productive White House strategy.

This underscores a wider point: whatever happens with coronavirus, the US has missed an opportunity, not just under Mr Trump but ever since the 2008 financial crisis, to reset its growth strategy, ideally to one based more on income growth than asset price inflation. That is the only way to assure economic security over the longer term.

China, too, has been overly dependent on debt during the post-financial crisis period. It has brewed up its own bubbles in everything from real estate to provincial bonds. Consumption and labour markets were weakening even before coronavirus hit. Trust in governance, already waning under President Xi Jinping, has taken a new hit with the party’s initial downplaying of the crisis.

And yet, whatever toll the virus may eventually take on global growth, the fact that recession fears, which seemed a non-issue only a week ago, are now back says something very important.

The US still matters a lot in the global economy, but much less than it used to. China, on the other hand, matters much more. Just how much will be measured as the story of coronavirus plays out in the weeks and months ahead.

[email protected]

Follow Rana Foroohar with myFT and on Twitter

Photo used under Creative Commons from the_donald_fotos